June 9, 2020

PPDocs system change: Modifications and Reg. Z, DocuSign Phishing Schemes Reported and more!

Read more below!

PPDocs system change: Modifications and Reg. Z (including tests found in Sections 32, 35, 43)

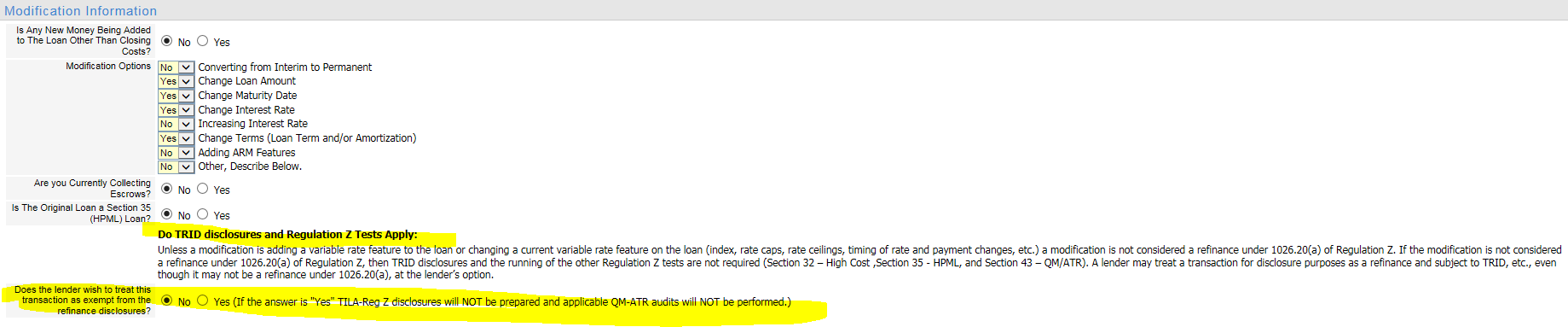

We updated the Modification Information screen to more clearly describe when a modification requires new TRID disclosures. The updates also more clearly ask lenders to indicate whether the modification being ordered should include new TRID disclosures and whether Reg.Z High Cost, HPML and QM/ATR tests should be run.

The language below now appears at the bottom of the Modification Information screen. Modifications that do not involve adding a variable rate feature or changing a variable rate feature are not considered refinances under Reg. Z and will not trigger TRID disclosures and the Reg. Z tests. However, a lender still has the option to deliver TRID disclosures on any modification at its discretion.

Do TRID disclosures and Regulation Z Tests Apply:

Unless a modification is adding a variable rate feature to the loan or changing a current variable rate feature on the loan (index, rate caps, rate ceilings, timing of rate and payment changes, etc.) a modification is not considered a refinance under 1026.20(a) of Regulation Z. If the modification is not considered a refinance under 1026.20(a) of Regulation Z, then TRID disclosures and the running of the other Regulation Z tests are not required (Section 32 – High Cost ,Section 35 - HPML, and Section 43 – QM/ATR). A lender may treat a transaction for disclosure purposes as a refinance and subject to TRID, etc., even though it may not be a refinance under 1026.20(a), at the lender’s option.

Now, if a lender wishes to exempt the modification from TRID disclosures and from running all of the Reg. Z tests, it may simply answer “Yes” that the transaction is considered exempt.

Please see reference here

{kind=link}

Notice of availability of revised CHARM Booklet

On June 3, 2020, the Bureau of Consumer Financial Protection (CFPB) announced the availability of an updated consumer publication, the Consumer Handbook on Adjustable Rate Mortgages booklet, also known as the CHARM booklet, required under RESPA implemented by Reg. X and TILA implemented by Reg. Z. This version of the CHARM booklet is updated to align with the CFPB’s educational efforts, to be more concise, and to improve readability and usability. The PPDocs system has been updated with the new CHARM Booklet. Federal Register notice. CHARM Booklet.

FTC: Free Credit Reports

According to a May 18, 2020, FTC blog, everyone is eligible to get free weekly credit reports from the three national credit reporting agencies: Equifax, Experian, and Transunion. To get your free reports, go to AnnualCreditReport.com. The credit reporting agencies are making these reports free for the next year.

CFPB and CSBS Release Guide to Mortgage Relief

To guide homeowners with federally backed loans through the process of obtaining mortgage relief, on May 15, 2020, the CFPB and the Conference of State Bank Supervisors released a Consumer Relief Guide with borrowers’ rights to mortgage payment forbearance and foreclosure protection under the federal CARES Act.

FHFA Announces Payment Deferral as New Repayment Option for Homeowners in COVID-19 Forbearance Plans

On May 13, 2020, to help homeowners who are in COVID-19 related forbearance, the Federal Housing Finance Agency (FHFA) announced that Fannie Mae and Freddie Mac (the GSE’s) made available a new payment deferral option. The payment deferral option allows borrowers who can return to making their normal monthly mortgage payment the ability to repay their missed payments at the time the home is sold, refinanced, or at maturity.

FHFA and the GSE’s do not require lump sum repayment at the end of the forbearance. Servicers are required to evaluate borrowers for one of several repayment options, generally referred to as a “hierarchy" of repayment and loan modification options.

Payment deferral is one of the repayment options. Payment deferral takes the missed mortgage payments and puts them into a payment due at the sale, or refinancing of the home, or the end of the loan. The borrower's monthly mortgage payment will not change. Mortgages that exercise the payment deferral option will remain in GSE Mortgage-Backed Securities, subject to the terms of the trust agreements.

Servicers will begin offering the payment deferral repayment option starting July 1, 2020. In addition to the new payment deferral option, borrowers with COVID-19-related hardships can still utilize other repayment options that include reinstatement, repayment plan, or loan modification, based on their individual situations.

Fannie Mae: Understand Your COVID-19 Mortgage Options

Freddie Mac: Lump Sum Repayment is Not Required in Forbearance

Fannie and Freddie extend foreclosure moratorium

On May 14, 2020, the Federal Housing Finance Agency announced that the GSEs were extending their moratorium on foreclosures and evictions until at least June 30, 2020. The foreclosure moratorium applies to GSE-backed, single-family mortgages only. The moratorium was set to expire on May 17th.

DocuSign Phishing Schemes Reported

There have been several reports of a DocuSign phishing attack during the pandemic. The reports say the attackers impersonate DocuSign emails and state there is a document for review from “CU #COVID19 Electronics Documents.” DocuSign has provided this information for detecting DocuSign-themed phishing attempts:

A few simple techniques can help you spot the difference between a spoofed DocuSign email and the real thing:

Don’t open unknown or suspicious attachments, or click links—DocuSign will never ask you to open a PDF, office document or zip file in an email

Hover over all embedded links: URLs to view or sign DocuSign documents contain “docusign.net/” and always start with https

Access your documents directly from www.docusign.com by entering the unique security code, which is included at the bottom of every DocuSign email

Report suspicious DocuSign-themed emails to your internal IT/security team and to spam@docusign.com

DocuSign provides advice on avoiding phishing scams: https://www.docusign.com/blog/docusign-update-recent-phishing-attack/

DocuSign on reporting suspicious incidents: https://www.docusign.com/trust/security/incident-reporting

June 2020 Frequently Asked Question

Question: Must both spouses receive the 12-day notices on a: 1) Texas home equity loan; and 2) Texas rate/term refinance of a home equity loan?

Answer:

Whether a lender is refinancing a home equity loan into a rate/term loan with no new funds advanced (F2) or refinancing it into another home equity loan (A6), the lender is only required to provide one copy of the 12-day notice to married owners. See 7 TAC §153.45(4)(E) (below) for an F2 rate/term refinance and 7 TAC §153.12 (below) for a refinance of an A6 loan into another A6 loan below.

However, in order to demonstrate compliance with the delivery and timing requirements for each 12-day notice in Texas Constitution, it is common and customary to: (1) require homestead owner signatures on the 12-day notice; and (2) have both spouses sign the 12-day notice on a home equity (even if one spouse is an non-borrowing spouse).

As with many things involving Texas home equity loans, the common and customary practices became the industry norm because they take the most conservative position to avoid the potentially draconian penalties associated with violating Texas home equity laws and regulations. Additionally, for secondary market loans, an investor may require both spouses receive and sign the 12-day notice. Accordingly, our default is to recommend that both spouses receive and sign the 12-day notice. In cases in which a loan closes and a lender subsequently tells us that the non-borrowing spouse did not receive and/or sign the 12-day notice, we typically cite the interpretation below and advise that it is probably not a major issue on a portfolio loan. On secondary market loans, of course, investor requirements will control.

7 Texas Admin. Code 153, Rule 153.45:

A refinance of debt secured by the homestead, any portion of which is an extension of credit described by Subsection (a)(6) of Section 50, may not be secured by a valid lien against the homestead unless either the refinance of the debt is an extension of credit described by Subsection (a)(6) or (a)(7) of Section 50, or all of the conditions in Section 50(f)(2) are met.

(4) Refinance Disclosure. To meet the condition in Section 50(f)(2)(D), the lender must provide the refinance disclosure described in Section 50(f)(2)(D) to the owner on a separate document not later than the third business day after the date the owner submits the loan application to the lender and at least 12 days before the date the refinance of the extension of credit is closed.

(E) One copy of the required refinance disclosure may be provided to married owners.

Source Note: The provisions of this §153.45 adopted to be effective March 29, 2018, 43 TexReg 1839

7 Texas Admin. Code 153, Rule 153.12:

An equity loan may not be closed before the 12th calendar day after the later of the date that the owner submits an application for the loan to the lender or the date that the lender provides the owner a copy of the required consumer disclosure. One copy of the required consumer disclosure may be provided to married owners. For purposes of determining the earliest permitted closing date, the next succeeding calendar day after the later of the date that the owner submits an application for the loan to the lender or the date that the lender provides the owner a copy of the required consumer disclosure is the first day of the 12-day waiting period. The equity loan may be closed at any time on or after the 12th calendar day after the later of the date that the owner submits an application for the loan to the lender or the date that the lender provides the owner a copy of the required consumer disclosure.

Source Note: The provisions of this §153.12 adopted to be effective January 8, 2004, 29 TexReg 84; amended to be effective November 13, 2008, 33 TexReg 9074